Why Some Buyers Get Rejected by Mortgage Lenders

Keeping Current Matters April 8, 2026

Buyer

Keeping Current Matters April 8, 2026

Buyer

One of the biggest reasons buyers do not make it to the finish line is financing.

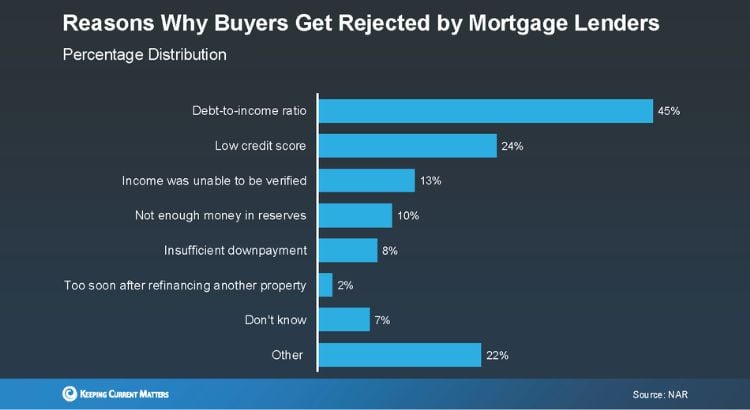

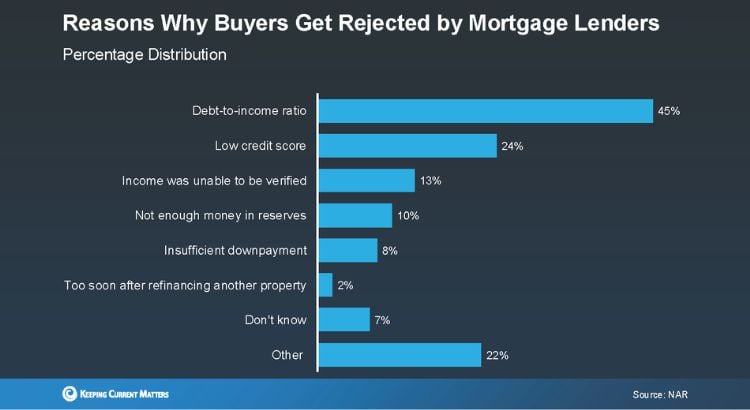

According to NAR, the most common reason buyers are rejected by mortgage lenders is their debt-to-income ratio, followed by low credit score, income that could not be verified, insufficient reserves, and not having enough down payment.

A buyer may have a strong income, but if too much of it is already committed to existing debt, a lender may decide the loan is too risky. Debt-to-income ratio is one of the biggest factors lenders consider because it helps show whether a buyer can realistically handle the monthly mortgage payment along with their other obligations.

Credit score also plays a major role in the approval process. A lower score can make it harder for a buyer to qualify for a mortgage, and even when approval is possible, it may come with less favorable loan terms.

Lenders want to see stable, verifiable income. If a buyer’s income cannot be fully documented or confirmed, that can delay the process or lead to a rejection. This is especially important for buyers with nontraditional income sources, self-employment income, or recent job changes.

In addition to the down payment and closing costs, lenders often want to see that buyers have extra funds set aside. These reserves help show that the buyer could continue making payments even if unexpected expenses come up.

A buyer may be financially close, but still fall short if they do not have enough saved for the required down payment. This can become a challenge even for otherwise qualified buyers, especially in higher-priced markets.

This is an important reminder for both buyers and sellers.

For buyers, preparation matters.

For sellers, working with well-qualified buyers matters just as much.

Understanding these financing challenges early can help avoid delays, disappointments, and deals falling out of contract.

Financing is one of the most important parts of any home purchase. The more prepared a buyer is before making an offer, the stronger their position can be. And for sellers, knowing that a buyer is truly qualified can make a meaningful difference in how confidently they move forward.

Attribution:

Source: Keeping Current Matters (KCM)

Additional source shown on slide: NAR

Stay up to date on the latest real estate trends.

Seller

July 23, 2026

Buyer

July 22, 2026

Buyer

July 20, 2026

Buyer

July 17, 2026

Seller

July 16, 2026

July 16, 2026

We Guide Homeowners through the complicated process of selling their home using our 4 Phase Selling Process and 3 Prong Marketing Strategy that alleviates their stress and moves them effortlessly to their next destination. Schedule a 15 Minute Complimentary Strategy Session Today